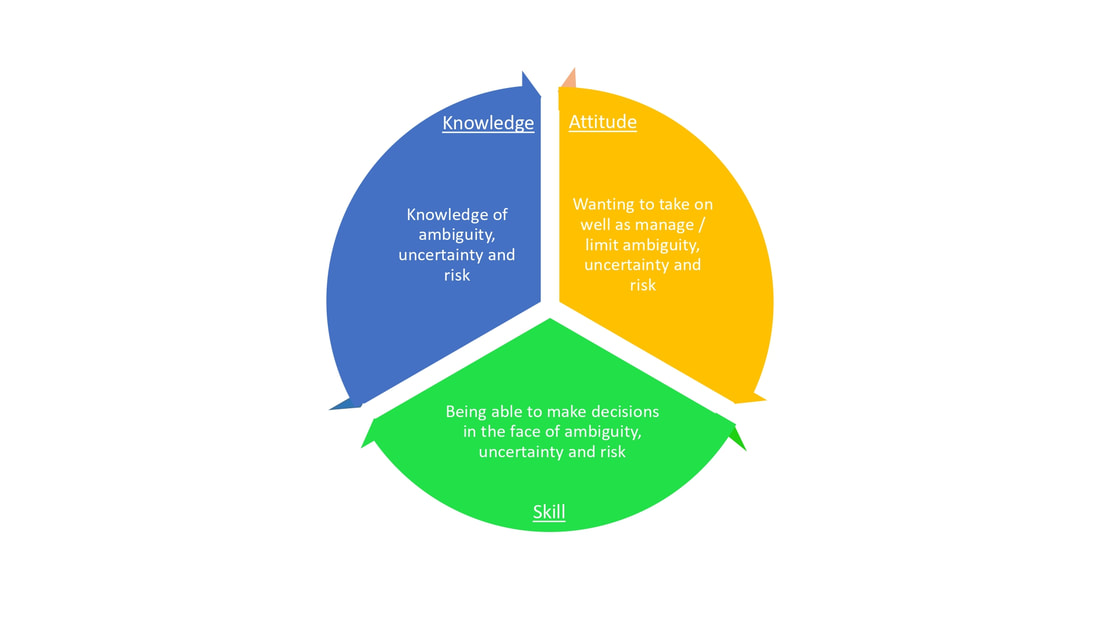

13 Coping with ambiguity, uncertainty and risk

13.1 Introduction

It was the Frenchman Richard Cantillon who, in the eighteenth century, first used the term 'entrepreneur'. He associated the term entrepreneur with risk-taking. His argument at the time was as follows: in addition to landowners and mercenaries, there is a third group of people active in the economy who distinguish themselves by their behavior rather than by their profession or social status. These people try to earn something at their own risk, for example by buying goods and selling them at a profit. According to Cantillon, these were the entrepreneurs. So taking risks and not knowing exactly what the outcome will be has been an important behaviour associated with business for centuries. Even today: if you ask students what behaviour they associate with entrepreneurs, risk-taking is often mentioned. A nice question as a teacher is: "If risk taking is so important, what is the difference between entrepreneurs and gamblers in a casino? After all, the latter group also behaves in a risky manner, don't they? After some hesitation, the answer is usually that entrepreneurs take different risks than gamblers. Entrepreneurs do not consider themselves such big risk takers, and certainly not gamblers, after all their ideas are based on plans, right? [see: Planning and management]. Yet statistics show that at least half of the new companies fail. What is going on here?

13.2 Insights

Risk appetite

Research on risk appetite has a rich history in entrepreneurship research. Although it remains difficult to compare different groups with each other, such as managers and entrepreneurs, meta-analyses do show that there is a direct relationship between risk appetite and entrepreneurial success [1]. However, it must be said that this relationship is not very strong; moreover, both are likely a function of intended firm size, in other words, ambition. Some caution is therefore in order when it comes to risk attitude. What makes it complicated is that there are differences in risk perception. Entrepreneurs may not have a high risk appetite in general (as gamblers do), but rather evaluate risks differently. It is therefore important to look at the decision strategies of entrepreneurs with regard to risks. Perhaps entrepreneurs are better able than others to manage and control risks. However, another way to look at this is from the perspective that entrepreneurs make decisions with certain cognitive biases, or in other words with certain distortions of reality [2]. We mentioned overconfidence earlier [see: Self-awareness and self-efficacy], but a 'sense of control' (in reality usually an illusion), and hasty generalisation (availability bias and representative bias) also play a role in risk perception. These fallacies seem to lower entrepreneurs' risk perception. Unlike managers, for example, entrepreneurs are more inclined to take decisions if certain information has not (yet) been taken into account, i.e. in situations characterised by ambiguity. Managers, for example, will be less inclined to take such decisions because they first want to have the missing information before making a decision. It is not wrong to point out these well-known biases to budding entrepreneurs, errors that, incidentally, not only entrepreneurs make. You can do this - as is often done in educational programmes - by asking students to first work out their plans in more detail or to sketch out scenarios ("what happens if...") in order to gain a better insight into the possible business case [see: Planning and management].

Uncertainty

However, the strategy of collecting more data only works if more is already known about a problem and/or a solution. When there is uncertainty, this strategy is much more difficult to apply. Risk, ambiguity and uncertainty are therefore not the same, as the famous American economist Frank Knight already argued a century ago. Risks have a 'known' probability distribution (e.g. the probability of a meteorite hitting the earth), ambiguity involves a lack of knowledge or different ideas about how to tackle a problem, but uncertainty involves a lack of information simply because the future is unknown. Research into how entrepreneurs think and solve problems - research into effectuation - provides more insight into how entrepreneurs deal with uncertainty. The basis for this was laid in the influential research of Saras Sarasvathy [3]. It showed that experienced, successful entrepreneurs deal with uncertainty in their own unique way. In contrast to wanting to set boundaries around uncertainty and systemically evaluate the potential of the opportunity (what can I gain from it, including market and competition analysis), they choose the path of: what is it worth to me to get started and what am I willing to lose? What is the maximum risk I run? How can I reduce this as much as possible? Sarasvathy calls this the affordable loss principle. These entrepreneurs ultimately take decisions of which they personally feel that the advantages outweigh the disadvantages; if the action turns out to be wrong, it will not have large-scale consequences. Moreover, taking action may ultimately result in even more opportunities. From the (perhaps limited) resources that these entrepreneurs have at their disposal, they try to take as many actions as possible with as few risks as possible. Such reasoning is therefore always a personal consideration, not so much based on predictions and probability calculations, but on one's own situation, resources, possibilities, and thus risk appetite. It is not just about weighing up financial risks. Ultimately, the decision is not a hard calculation but is based on intuition or gut feeling, informed by experience.

Research on risk appetite has a rich history in entrepreneurship research. Although it remains difficult to compare different groups with each other, such as managers and entrepreneurs, meta-analyses do show that there is a direct relationship between risk appetite and entrepreneurial success [1]. However, it must be said that this relationship is not very strong; moreover, both are likely a function of intended firm size, in other words, ambition. Some caution is therefore in order when it comes to risk attitude. What makes it complicated is that there are differences in risk perception. Entrepreneurs may not have a high risk appetite in general (as gamblers do), but rather evaluate risks differently. It is therefore important to look at the decision strategies of entrepreneurs with regard to risks. Perhaps entrepreneurs are better able than others to manage and control risks. However, another way to look at this is from the perspective that entrepreneurs make decisions with certain cognitive biases, or in other words with certain distortions of reality [2]. We mentioned overconfidence earlier [see: Self-awareness and self-efficacy], but a 'sense of control' (in reality usually an illusion), and hasty generalisation (availability bias and representative bias) also play a role in risk perception. These fallacies seem to lower entrepreneurs' risk perception. Unlike managers, for example, entrepreneurs are more inclined to take decisions if certain information has not (yet) been taken into account, i.e. in situations characterised by ambiguity. Managers, for example, will be less inclined to take such decisions because they first want to have the missing information before making a decision. It is not wrong to point out these well-known biases to budding entrepreneurs, errors that, incidentally, not only entrepreneurs make. You can do this - as is often done in educational programmes - by asking students to first work out their plans in more detail or to sketch out scenarios ("what happens if...") in order to gain a better insight into the possible business case [see: Planning and management].

Uncertainty

However, the strategy of collecting more data only works if more is already known about a problem and/or a solution. When there is uncertainty, this strategy is much more difficult to apply. Risk, ambiguity and uncertainty are therefore not the same, as the famous American economist Frank Knight already argued a century ago. Risks have a 'known' probability distribution (e.g. the probability of a meteorite hitting the earth), ambiguity involves a lack of knowledge or different ideas about how to tackle a problem, but uncertainty involves a lack of information simply because the future is unknown. Research into how entrepreneurs think and solve problems - research into effectuation - provides more insight into how entrepreneurs deal with uncertainty. The basis for this was laid in the influential research of Saras Sarasvathy [3]. It showed that experienced, successful entrepreneurs deal with uncertainty in their own unique way. In contrast to wanting to set boundaries around uncertainty and systemically evaluate the potential of the opportunity (what can I gain from it, including market and competition analysis), they choose the path of: what is it worth to me to get started and what am I willing to lose? What is the maximum risk I run? How can I reduce this as much as possible? Sarasvathy calls this the affordable loss principle. These entrepreneurs ultimately take decisions of which they personally feel that the advantages outweigh the disadvantages; if the action turns out to be wrong, it will not have large-scale consequences. Moreover, taking action may ultimately result in even more opportunities. From the (perhaps limited) resources that these entrepreneurs have at their disposal, they try to take as many actions as possible with as few risks as possible. Such reasoning is therefore always a personal consideration, not so much based on predictions and probability calculations, but on one's own situation, resources, possibilities, and thus risk appetite. It is not just about weighing up financial risks. Ultimately, the decision is not a hard calculation but is based on intuition or gut feeling, informed by experience.

13.3 Further reading

[1] In this article, psychologists Michael Frese and Michael Gielnik combined the results of separate studies on characteristics of entrepreneurs and success into an 'overall' result. Risk taking is one of those characteristics. They conclude that the risk appetite of entrepreneurs is higher than that of managers, and that the risk appetite of entrepreneurs who want to grow is higher than that of entrepreneurs who are focused on a stable income. Frese, M., & Gielnik, M.M. (2014). The psychology of entrepreneurship. Annual Review of Organizational Psychology and Organizational Behavior, 1(1), 413-438.

[2] Olivier Thomas listed 54 scientific articles around thinking errors in entrepreneurship. The main conclusion is that the scientific evidence was strongest and most consistent for the role of optimism and self-aggrandizement. Entrepreneurs are generally optimists, with the majority even being extremely optimistic. Thomas, O. (2018). Two decades of cognitive bias research in entrepreneurship: what do we know and where do we go from here? Management Review Quarterly, 68(2), 107-143.

[3] In a famous 2001 article, Saras Sarasvathy lays the foundation for studying how entrepreneurs think by means of two thought experiments. Sarasvathy, S.D. (2001). Causation and effectuation: Toward a theoretical shift from economic inevitability to entrepreneurial contingency. Academy of Management Review, 26(2), 243-263.

[4] Report on an educational innovation to start the conversation in the classroom about thinking errors in entrepreneurship. Michaelis, T. L., Pollack, J. M., Mulvey, P., Ritter, B. M., & Carr, J. C. (2020). Gender bias and venture funding: discussing bias in the entrepreneurship classroom. Entrepreneurship Education and Pedagogy, 3(2), 154-181.

[2] Olivier Thomas listed 54 scientific articles around thinking errors in entrepreneurship. The main conclusion is that the scientific evidence was strongest and most consistent for the role of optimism and self-aggrandizement. Entrepreneurs are generally optimists, with the majority even being extremely optimistic. Thomas, O. (2018). Two decades of cognitive bias research in entrepreneurship: what do we know and where do we go from here? Management Review Quarterly, 68(2), 107-143.

[3] In a famous 2001 article, Saras Sarasvathy lays the foundation for studying how entrepreneurs think by means of two thought experiments. Sarasvathy, S.D. (2001). Causation and effectuation: Toward a theoretical shift from economic inevitability to entrepreneurial contingency. Academy of Management Review, 26(2), 243-263.

[4] Report on an educational innovation to start the conversation in the classroom about thinking errors in entrepreneurship. Michaelis, T. L., Pollack, J. M., Mulvey, P., Ritter, B. M., & Carr, J. C. (2020). Gender bias and venture funding: discussing bias in the entrepreneurship classroom. Entrepreneurship Education and Pedagogy, 3(2), 154-181.

13.4 Exercises for students

1) Risk and uncertainty

Students are asked to bring three PET bottles, a bag of candy with different types of candy and black paint (or Duct tape). The neck of the first PET bottle is cut off and then students are asked to empty the bag of candy into the bottle. The students are then asked what the distribution is full/empty. Because the bottle is transparent and they can see the colours of the candy, they can estimate the distribution quite well (for example 80/20). Now the teacher asks them to paint the second bottle black (or wrap it with Duct tape), and put the second bag of candy in it. Again, the teacher asks what the division is. Because students cannot see now, they will have to estimate what the distribution is based on, for example, a sample. Finally the teacher fills the third bottle, which is also painted black. He no longer fills the bottle with sweets, but with all kinds of different objects (e.g. stapler, pen, stones). Now it is impossible to estimate what is in the bottle. This is what uncertainty is.

Explanation: Risk and uncertainty are different concepts and it is important to distinguish them. This exercise - based on an exercise from effectuation.org - makes the differences immediately clear and shows that linear thinking (think of making estimates in business plans, for example) becomes more difficult as uncertainty increases.

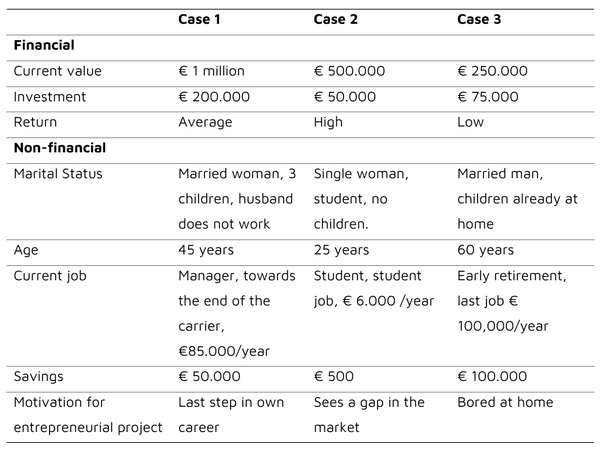

2) Minicase: affordable loss principle

Students work in groups on the question 'In which person's shoes would you like to be'? On the basis of which considerations? The decision will likely not be based on the financial data only. What could be additional resources?

Students are asked to bring three PET bottles, a bag of candy with different types of candy and black paint (or Duct tape). The neck of the first PET bottle is cut off and then students are asked to empty the bag of candy into the bottle. The students are then asked what the distribution is full/empty. Because the bottle is transparent and they can see the colours of the candy, they can estimate the distribution quite well (for example 80/20). Now the teacher asks them to paint the second bottle black (or wrap it with Duct tape), and put the second bag of candy in it. Again, the teacher asks what the division is. Because students cannot see now, they will have to estimate what the distribution is based on, for example, a sample. Finally the teacher fills the third bottle, which is also painted black. He no longer fills the bottle with sweets, but with all kinds of different objects (e.g. stapler, pen, stones). Now it is impossible to estimate what is in the bottle. This is what uncertainty is.

Explanation: Risk and uncertainty are different concepts and it is important to distinguish them. This exercise - based on an exercise from effectuation.org - makes the differences immediately clear and shows that linear thinking (think of making estimates in business plans, for example) becomes more difficult as uncertainty increases.

2) Minicase: affordable loss principle

Students work in groups on the question 'In which person's shoes would you like to be'? On the basis of which considerations? The decision will likely not be based on the financial data only. What could be additional resources?

Explanation: This mini-case - based on effectuation.org - can be built up differently depending on the students and the course, the examples are only indicative. The case is also a stepping stone for students who are already engaged in entrepreneurial projects, such as a mini-company, a hobby project or idea development, to ask the question: what is the maximum risk you run? How much are you prepared to commit all your available resources, what are you prepared to lose? For example, how bad would it be if you ended up in the newspaper? What is an affordable loss in your personal situation?

3) Thinking mistakes

In this assignment the students give a summary of a new (business) idea of an entrepreneur. This can be an (existing) idea from the region, from school, as long as it is new to the group. There are three versions of this. In the first version the idea is written by a female entrepreneur (use of 'she'), in the second version by a man (use of 'he') and in the last version the piece is gender neutral. Students are asked in groups what they think of the idea and whether they would invest in it. Students are asked what they notice about the idea/project and what was important in deciding whether or not to invest. Each group gets a different version. Afterwards the groups discuss whether gender has played a role in the group and in deciding whether or not to invest in the idea.

Explanation: This assignment is meant as a stepping stone to how 'unconscious factors' play a role in decisions within entrepreneurship. Plenary can be discussed how other 'thinking biases’ also play a role in decisions, such as overconfidence and optimism. This exercise is based on the experiment of Timothy Michaelis and colleagues [4].

3) Thinking mistakes

In this assignment the students give a summary of a new (business) idea of an entrepreneur. This can be an (existing) idea from the region, from school, as long as it is new to the group. There are three versions of this. In the first version the idea is written by a female entrepreneur (use of 'she'), in the second version by a man (use of 'he') and in the last version the piece is gender neutral. Students are asked in groups what they think of the idea and whether they would invest in it. Students are asked what they notice about the idea/project and what was important in deciding whether or not to invest. Each group gets a different version. Afterwards the groups discuss whether gender has played a role in the group and in deciding whether or not to invest in the idea.

Explanation: This assignment is meant as a stepping stone to how 'unconscious factors' play a role in decisions within entrepreneurship. Plenary can be discussed how other 'thinking biases’ also play a role in decisions, such as overconfidence and optimism. This exercise is based on the experiment of Timothy Michaelis and colleagues [4].

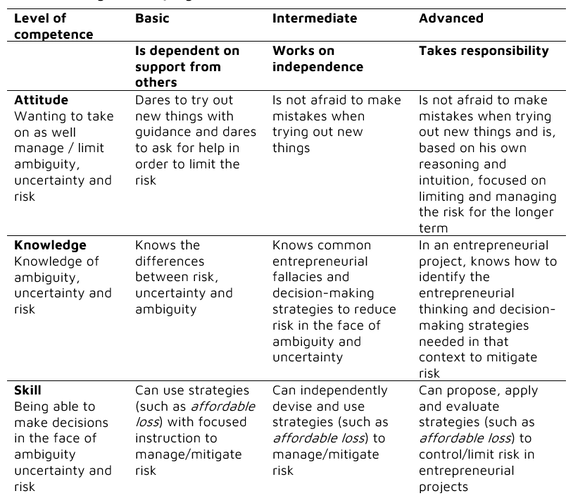

13.5 Measuring student progress